Wednesday, March 10, 2021

Costanza repeatedly “diss” by Edgar County Watchdog

![]()

![]()

Support

Our Mission

MARCH 10, 2021

FEATURE, POPLAR GROVE

Poplar Grove Candidate’s Run-in with Insurance Licenses In Three States -

BY JOHN KRAFT & KIRK ALLEN

POPLAR GROVE, IL. (ECWd) -

Update: Owen Costanza responded to this article: (Read it here)

Mayoral Candidate’s Run-in with Insurance Licenses In Three States: Fined $31,500

When a candidate, any candidate, touts their public service and their honesty, without revealing the truth in their past dealings with state regulatory agencies, we believe the people have a right to know.

Such is the case with Owen Costanza, current Mayor, and 2021 Mayoral Candidate, for the Village of Poplar Grove.

His campaign webpage talks about his “work ethic” and applying his business management experience to village operations.

Below, we discuss his “work ethic” and “business management experience” as observed through the eyes of Insurance regulators in Indiana, Wisconsin, and Illinois.

Some of this includes lying on applications for business insurance licenses by failing to disclose criminal convictions and failing to disclose termination of his company for allegations of misconduct. Paying civil penalties of $31,500.00 to various state departments of insurance, failing to tender paid premiums to insurance providers, and improper withdrawals from several accounts, among others.

We have asked Owen Costanza to provide comments on these issues, he has yet to respond.

ILLINOIS

On February 18, 2015, a “STIPULATION AND CONSENT ORDER” was signed by Costanza, Licensee and representative of RMS Service Group, Inc., d/b/a as Alliance Insurance Agency, which supersedes the Order of Revocation dated April 3, 2014. This matter was on the Revocation of licensing authority of RMS Service Group d/b/a as Alliance Insurance Agency

In this signed ORDER:

- Respondent shall pay a civil penalty of $30,000 to the Director of the Illinois Department of Insurance

- Voluntarily agree to revocation of the Business Entity license of RMS Service Group, Inc. d/b/a/ as Alliance Insurance Agency

- The Premium Fund Trust Account (“PTFA”) was deficient for 117 days and pertained to 17 consumers, ranging from $200.14 to $24,574.16 with an average of $15,240.35

- Collected insurance premiums from three customers between Aug 2, 2010 and Oct 21, 2010, and failed to forward the premiums to the insurer within the required timeframe – holding four premiums for an average of 301 days

- During March 2010, made unlawful withdrawals totaling $9,400 from the PTFA account, $10,733.97 from the Main account, and $16,385.66 from the Operating account

- On Sep 22, 2010, deposited $365.83 from a consumer for homeowner’s insurance policy, then paid the insurer $196.40, but did not repay the $169.43 to the consumer until more than a year later

- Charging service fees without a service fee agreement

- Check register did not include positive running balances after each deposit or disbursement – and had a negative balance on 32 separate dates

- Maintaining a Bond of $2500.00 when, in 2010, the minimum amount of the Bond for 2011 should have been $7342.00

- Failed to disclose the 2008 denial of a Business Entity and Licensee’s application in the State of Wisconsin for failing to disclose previous criminal convictions on an insurance license application and failing to disclose a company termination for allegations of misconduct

- Failed to disclose the 2010 State of Indiana civil penalty against the Licensee for failing to disclose previous criminal convictions, having judgment withheld or deferred, pending criminal investigation, or being named in an administrative proceeding

- Falsely answered “NO” to question #2 of the application about their involvement in an administrative proceeding, regarding whether administrative action was taken by another State on their 2010 and 2012 application for renewals for a license

- Conducting business in a name other than the name on the license issued for a Business Entity

- Check register examined by the Department did not have all check issues listed and was not accurate as the actual checks issued with the correct check number

- Other issues with listings of deposits or monies received

- No bank reconciliations between 2008 and 2011

- Bank accounts listed as Premium Trust Account and a check was written from that account on Sep 9, 2010 (we cannot locate any more information about this check to report who it was written to)

INDIANA

On September 21, 2010, the Indiana Commissioner of Insurance filed a “FINAL ORDER AND APPROVAL” and another filing labeled “AGREED ENTRY” in Cause Number 9384-AG10-0831-135, which is labeled as “Enforcement Action” naming Owen Costanza as the Agent/Respondent to Indiana Insurance License Number 425943.

In the signed filings for this Cause:

- Respondent shall pay a $1500 civil penalty to the Indiana Department of Insurance

- Respondent falsely indicated “NO” to the question of whether he had ever been convicted of a crime, had a judgment withheld or deferred, or was currently charged with committing a crime

- Respondent falsely indicated “NO” to the question of whether he had ever been named as a party in an administrative proceeding regarding any professional or occupational license or registration

- Respondent falsely indicated “NO” to the question of whether he had ever had an insurance agency contract or any business relationship with an insurance company terminated for any alleged misconduct

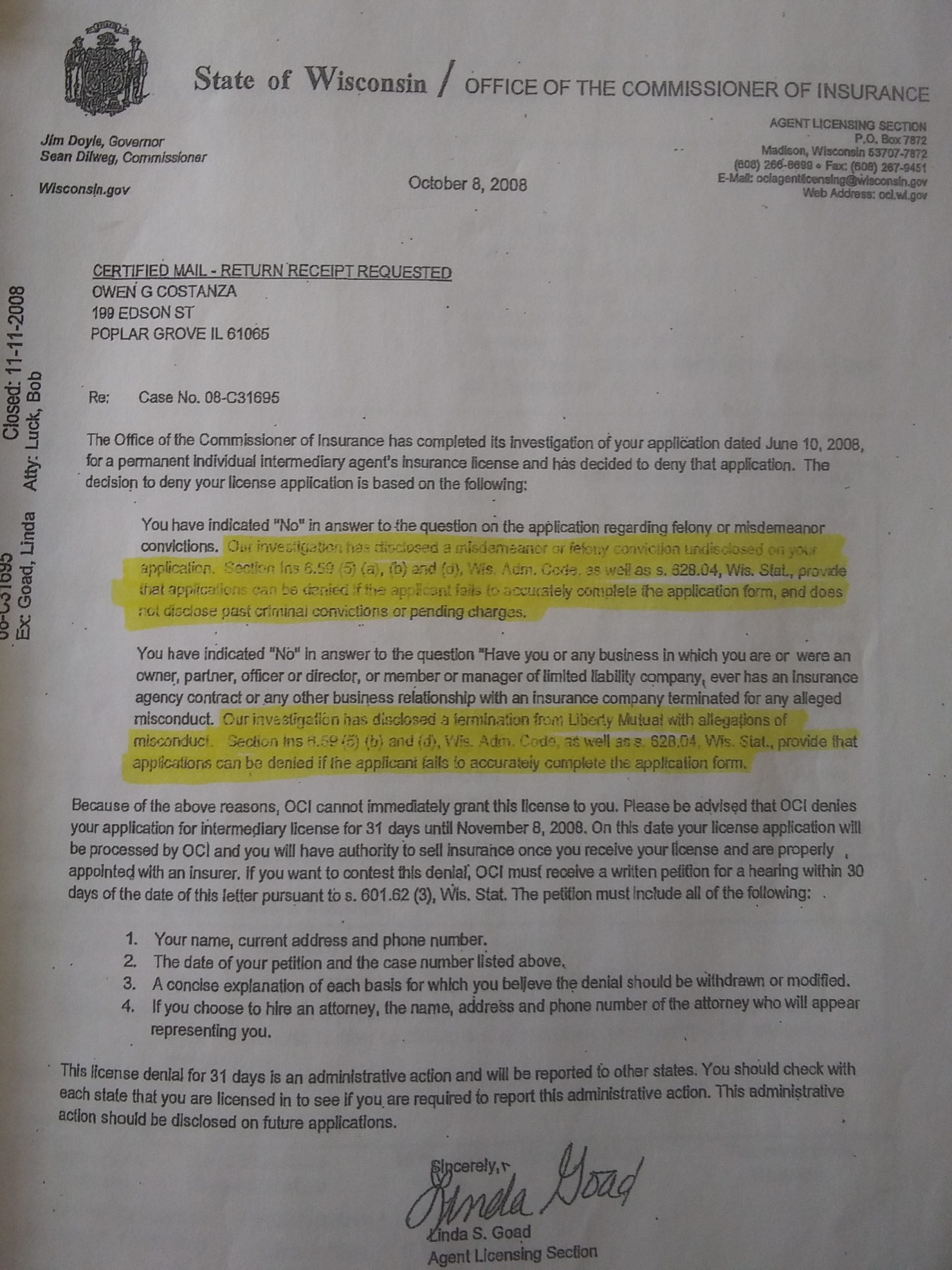

WISCONSIN

- Licensed DENIED for 31 days based on allegations of failing to disclose previous criminal convictions on an insurance license application and failing to disclose a company termination for allegations of misconduct. November 2008 (See page 41

**************************************************************************************************************************************

Search

MARCH 10, 2021

FEATURE, POPLAR GROVE

Owen Costanza's Response Misleading; Doesn't Match Public Records -

BY JOHN KRAFT & KIRK ALLEN

POPLAR GROVE, IL. (ECWd) -

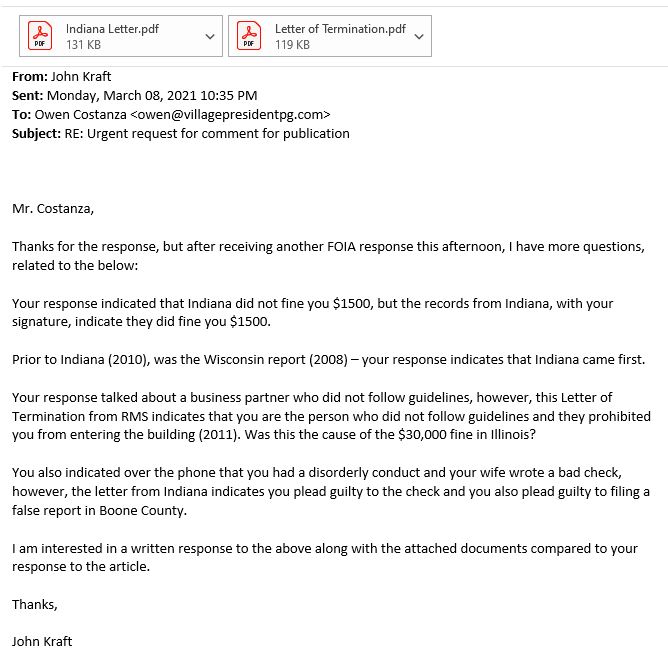

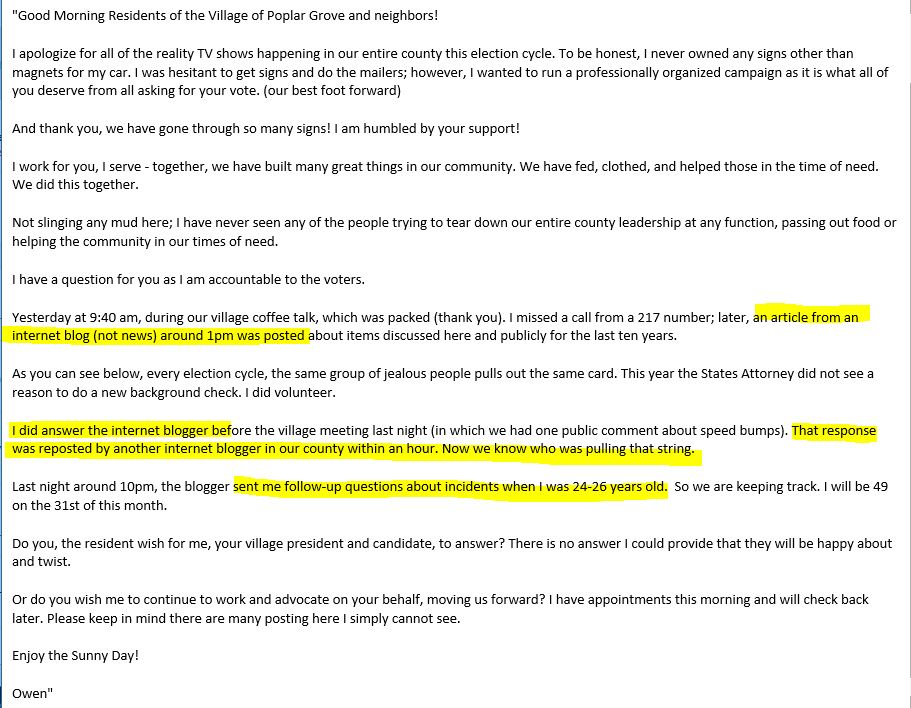

Yesterday we published complaints against Owen Costanza by the Illinois, Indiana, and Wisconsin State Insurance Licensing Regulators, and Costanza responded with his version of what he was willing to tell us.

These were as recent as 2011 and 2015 (Stipulation and Consent Order) - not things that happened "in his 20s".

The problem is, his response does not match with public records obtained from state regulatory agencies.

Last night I sent him follow-up questions, but instead of answering them, he took to social media to gain sympathy and peddle misinformation. In the social media post, he conveniently "forgets" to mention the most important part of the questions I sent him, which was the Letter of Termination, his blaming other people, and his claims of disorderly conduct instead of what it actually was.

In Costanza's response letter to our article:

- he blamed employees for "accidentally" lying on the license applications in two states

- claimed the conviction was a "disorderly conduct" when he was 24 years old

- he blamed a business partner on his issues in Illinois, claiming the business partner did not follow guidelines and there was money that needed to be replaced, and since he [Costanza] was the one with the license, he was the one responsible

In the FOIA responses:

- Indiana Director of Fraud Investigations sent a letter detailing Costanza's convictions, which include:

- pleading guilty to false reporting in 1995 in Boone County (withhold judgment)

- pleading guilty to writing a bad check in 1999 in Boone County

- terminated for cause in 1995 from Liberty Mutual with allegations that he filed a false insurance claim - and also noted that the Illinois Department of Unemployment Insurance ruled there was insufficient evidence to support the allegation

- that Costanza's 2008 application for insurance license in Wisconsin was denied for 31 days for failure to disclose the criminal convictions and for failing to disclose his termination for cause from Liberty Mutual

- RMS Service Group issued a Letter of Termination to Costanza in 2011 (related to the $30,000 penalty from Illinois) accusing him of the following:

- immediately terminating Costanza's employment with RMS Service Group, effective January 27, 2011

- that Costanza altered access to the Applied Systems TAM application, access to the phones, and changed company passwords at their insurance company databases

- that Costanza opened an unauthorized business account at Poplar Grove State Bank

- that Costanza conducted a mass deletion of emails without permission or authorization

- that these actions were done following being confronted on January 15, 2011, with unauthorized disbursements made to [Costanza] and on Costanza's behalf from the Premium Fund Trust Account maintained at National City Bank

- that he was confronted with and asked to explain altered customer premiums that did not reconcile with insurance policies issued to said customers

- that he formed RMS Insurance Services, Inc. on January 16, 2011, in Poplar Grove and that the RMS Service Group will make sure [Costanza] is held personally liable for any misappropriation of confidential information or trade secrets from it

- that Costanza is no longer permitted to enter the premises of the company unless escorted by Rashid Sindhu

These are the two vastly differing explanations about his dealings with the State of Illinois Insurance Licensing regulators and his dealings with his past employer.

Just look at the timeline on his termination letter from his employer:

- January 15, 2011 Costanza is confronted with certain evidence against him

- January 16, 2011 Costanza starts a new company with a similar name as his current employer's company

- January 27, 2011 Costanza received the termination letter

Add to that, the State of Illinois Department of Insurance investigation against him, which ended with a $30,000 civil penalty and voluntary revocation of his Business Entity License. This investigation and resolution closely align with the Letter of Termination.

All we asked for was honest responses, and after further review, his response was far from honest.

We ask you, our readers, to click on the links provided and read the documents for yourselves.

Above is from: https://edgarcountywatchdogs.com/2021/03/owen-costanzas-response-misleading-doesnt-match-public-records/?highlight=Owen%20Costanza

*********************************************************************************************************************************************************

Search

MARCH 10, 2021

FEATURE, POPLAR GROVE

Village of Poplar Grove's Electioneering Communications -

BY JOHN KRAFT & KIRK ALLEN

Poplar Grove, IL. (ECWd) -

It has come to our attention that the Village of Poplar Grove has been using its official Facebook page for electioneering purposes - in favor of the current Village President, Owen Costanza.

Use of official government communications, like email and social media, for electioneering purposes, is wrong and we urge residents of Poplar Grove to file an official complaint to either the Village's Ethics Commission (if there is one) or the Illinois State Board of Elections.

This gives an unfair disadvantage to other candidates and gives the impression that the Village is taking sides in the upcoming election. No amount of couching it as an informative listening session or "coffee talk" while advertising it as a "Re-elect Costanza" event could bring it into compliance.

These advertisements also pulled Illinois State Representative Joe Sosnowski into the electioneering issue, since his name is listed as a speaker at this event. He should have known better.

Screencaps of electioneering communications on Poplar Grove's official Facebook page:

{kind=link}

{kind=link}

{kind=link}

Above is from: https://edgarcountywatchdogs.com/2021/03/village-of-poplar-groves-electioneering-communications/?highlight=Owen%20Costanza

Subscribe to:

Posts (Atom)